Last year, Zhenghan Law Firm released a brief news item — “The Firm Won a Second-Instance Reversal at a High People’s Court in a Private Equity Fund Exit Dispute”. The second-instance judgment of this case successfully reversed the determination of “equity in name but debt in substance”, holding that in private equity investments, which contain both equity investment elements and debt financing characteristics, the transaction is different from a typical loan contract or investment contract, and should not and does not need to be defined as a contract of a single legal nature.

On the same day, many readers hoped to learn about the reasoning details through colleagues in the firm or messages on the backend, which shows the great importance of the word “exit” for investment institutions at present. Today, we will expand on this

Case Review: An Extremely Common Fund Investment and

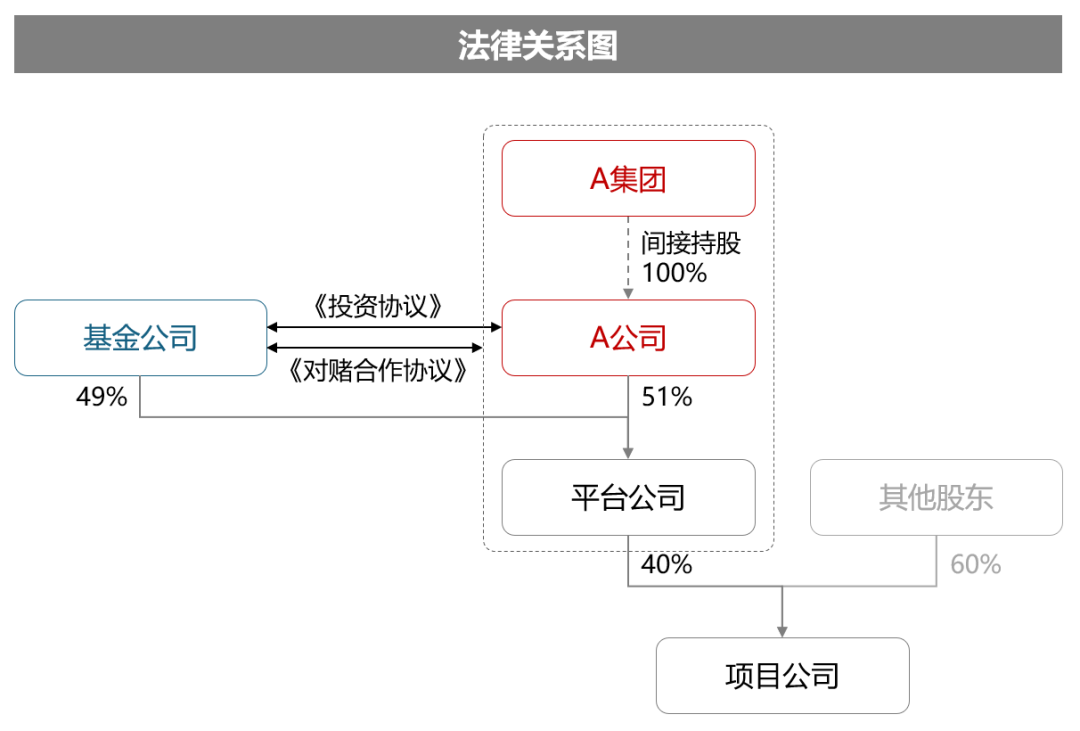

The fund company, through capital increase, jointly held shares in an investment platform with partner Company A. The investment funds were injected into the platform company in the form of registered capital and capital reserve, and finally invested in underlying projects.

The two parties agreed on a performance bet on the project company. The fund had the right to initiate a simulated liquidation when the investment period expired for 12 months, and require Company A (if the bet was successful) or Group A (if the bet was failed) to acquire the equity held by the fund at the consideration of the principal investment plus a relatively fixed investment return rate to realize exit.

After reading the case, I believe most readers will think this is an extremely common fund investment model with a clear and definite basis for claim rights. But at the same time, it is foreseeable that the most likely defense argument put forward by Company A and the core focus of the dispute are:Does the transaction in question constitute “equity in name but debt in substance

Regarding

First Instance Held: This Case Should Be Regulated by the Legal Relationship of Loan Contract

The main reasoning of the first-instance court was:

1. The essential difference between equity and debt investment lies in whether to bear the business risks of the enterprise, but the fund income in this case has nothing to do with the specific valuation of the project;

2. Going through industrial and commercial registration, enjoying shareholder voting rights, and participating in part of the actual operation and management may be measures taken by the investor to ensure capital safety, not the decisive factor affecting the determination of equity or debt;

3. The “Several Provisions on Strengthening the Supervision of Private Investment Funds” issued by the CSRC is a departmental normative document, and violating this provision is not sufficient to negate the validity of the loan contract.

Second Instance Held: It Should Not and Does Not Need to Be Defined as a Contract of a Single

The main reasoning of the second-instance court was:

1. The transaction in question is jointly composed of multiple agreements. The repurchase subject is different when the bet is successful or failed. In addition to the clauses agreeing on capital increase and share expansion and equity repurchase between shareholders, it also agrees on a large number of clauses involving corporate governance. These clauses are of great significance for all parties to sign and perform the contract. Especially for the fund, if such clauses are not binding, it is impossible for it to sign the transaction contracts involved;

2. After the signing of the contract, the fund acted as a shareholder and director in accordance with the agreement and essentially participated in the company’s operation and management. The purpose of the fund’s participation in the company’s internal governance is the same as that of other shareholders, which is to manage the company for the company’s interests, ensure the safety and profitability of the company’s assets, and then obtain investment returns;

3. In the case where the law does not prohibit parties from signing mixed contracts or atypical contracts, the agreements involved do not violate the prohibitive provisions of the law and there are no statutory invalid circumstances. Therefore, the court should still confirm its contract validity and respect the content of the contract clauses agreed by all parties based on autonomyOn the surface, the second instance only corrected the determination of the contract nature, which does not affect the amount of money payment, but practitioners in the private equity fund industry should deeply understand the importance of such a

1. It avoided the possible administrative penalties for the fund manager and key persons in charge;

2. It prevented fund investors from claiming that the fund company should fully refund the investment funds on the grounds of wrong investment direction and fundamental breach of contract (there have been such effective precedents);

3. The business of similar transaction models can continue to be carried out, and they dare to sue for exit.

Then, how did Zhenghan Law Firm lawyers achieve turning defeat

Case Highlights: Comprehensive Application1. Handle this case as a

Private equity fund investment exit disputes are of course financial disputes, but the issue of “equity in name but debt in substance” involved needs to draw on the rules and legal principles for determining shareholder qualifications in company law.

After realizing this point, this case must not be simply discussed on the grounds that “the contract has clear repurchase agreements”. It is also necessary to fully present evidence around the company’s articles of association, shareholder register, industrial and commercial registration, financial statements, internal company decision-making and management processes, etc., and then explain the viewpoints in combination with company law theories such as the three capital principles and2. Exhaustive

In cases involving the issue of “equity in name but debt in substance”, there are considerable differences in the judgment standards of individual cases, which is also a difficulty in handling this case.

When submitting the search report to the court, we did not avoid precedents that determined it as debt, but conducted an exhaustive search of all cases involving this issue in domestic financial courts, high people’s courts and the Supreme People’s Court, then conducted in-depth analysis of the similarities and differences with this case one by one, and tried to summarize the core criteria for distinguishing equity and debt, namely: fixed income exit is only a prerequisite for discussing the distinction between equity and debt, not the judgment standard for distinguishing equity and debt; if there is no agreement on fixed income, there is no need to discuss the distinction between equity and debt at all; actual participation in the company’s operation and management is the core standard for distinguishing equity and3. Take trial concepts and principles as important entry points for reasoning

The first instance of this case broke through the superficial investment agreement and essentially determined the transaction involved as private lending, which can be described as a typical example of “penetrating trial thinking”. However, the boundary of penetrating trial thinking and how to balance it with the basic principle of autonomy of will of parties are actually worthy of in-depth discussion.

Based on the analysis of this issue by a large number of judges, experts and scholars, we believe that penetrating trial thinking should be applied in a modest manner, especially when it does not involve contract validity, does not involve external relations but only affects both parties to the transaction, and does not involve civil relations but belongs to commercial transactions, we should avoid “excessive penetration” and “random penetration”.

In fact, in addition to clarifying the legal review rules for private equity investments, the second-instance agency of this case also achieved two important results worthy of mention:

First of all, in addition to Company A being ordered to bear the payment liability, the wholly-owned shareholder of Company A was also ordered to bear joint and several liability. This benefit from the application and proof of the relevant provisions on disregard of corporate personality in company law.

Secondly, the agreement involved has a clause that “a breach of contract by Company A shall be deemed a breach of contract by Group A”. The first-instance court determined this as a debt accession by Group A, but since Group A is a listed company and did not announce and disclose the transaction involved, it did not bear any compensation liability.

The second-instance court held that according to the transaction arrangement: if Company A fails to perform, Group A is obligated to transfer the equity involved. Therefore, the legal relationship between Group A and the fund is bilateral and remunerative, not subsequent debt accession. In view of this, the liability that Group A is obligated to bear in accordance with the contract should not be determined as guarantee or debt accession, and naturally there is no need to consider whether it is announced or not. Finally, the judgment was reversed to support all the fund’s claims against Group A.

The above litigation results are of great significance for the fund to expand the scope of recovery and improve the possibility of compensation recovery, and also have reference significance in other cases involving disregard of corporate personality, guarantee or quasi-guarantee validity.

The realization of these results all involves the demonstration of independent legal issues, but due to space limitations, today we only clarify the issue of distinguishing equity and debt, and the others will be put aside for the time being.